SMM July 10 News:

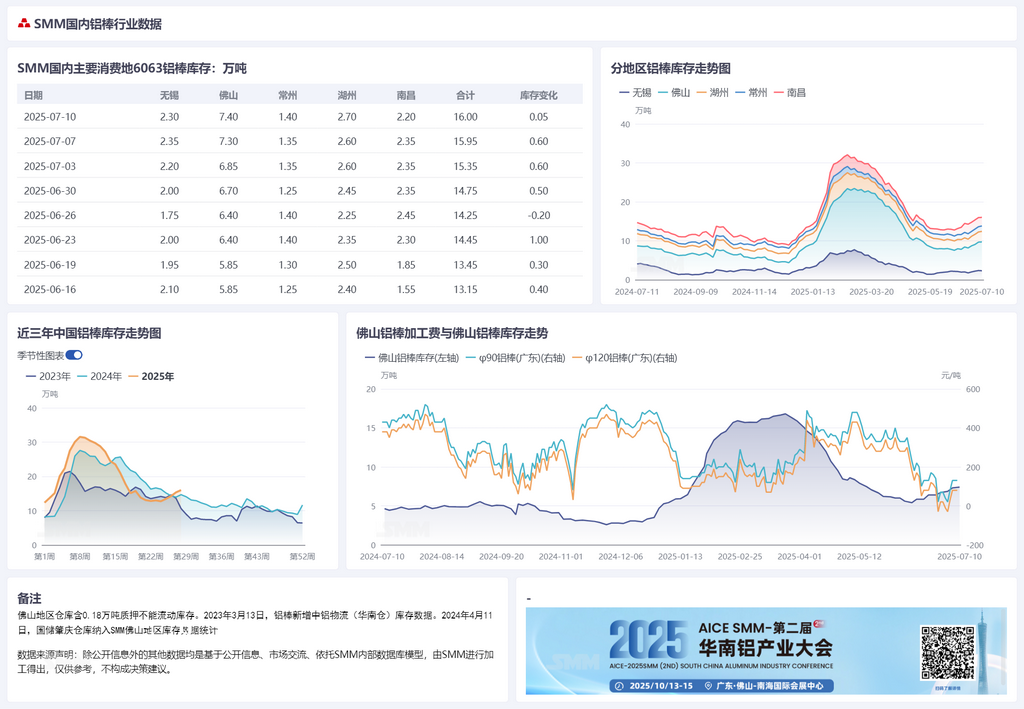

Regarding aluminum billet inventory, according to SMM statistics, on July 10, the inventory of aluminum billets in major domestic consumption areas was 160,000 mt, an increase of 500 mt from Monday and up 6,500 mt WoW from last Thursday. Since mid-June, when the inventory buildup turning point was established, the inventory level has continued to rise, reaching the highest position in three years for the same period, reflecting the increasingly heavy pressure on the supply side of aluminum billets. By region, the Foshan market, due to the continuous weakening of demand and the continuous arrival of goods in storage, became the main area for domestic inventory increases; the Wuxi area also saw an increase in inventory due to the weakening of just-in-time procurement of extrusions in surrounding areas; the Nanchang area, however, experienced a slight destocking due to the recovery of the Guangdong-Shanghai price spread and fewer arrivals. Although there are reports of production cuts by some aluminum billet manufacturers, the off-season combined with high temperatures severely impacted downstream just-in-time procurement, so the current production cuts by aluminum billet manufacturers cannot stop the inventory buildup.

In terms of aluminum billet consumption, SMM statistics show that during the 6.3-7.6 period, the total outflows from warehouses of aluminum billets in China were 34,800 mt, down 2,400 mt WoW. From the data on aluminum billet outflows, it can be seen that overall market consumption is still on a downward trend, with weak new orders and the early consumption driven by the PV installation rush in H1, leading to unclear market consumption confidence. It is expected that subsequent outflows from warehouses of aluminum billets will continue to operate at low levels. Overall, the pressure on the supply side of aluminum billets is still gradually increasing, while the sentiment on the demand side remains cautious and unable to scale up. SMM expects that aluminum billet inventory will continue to maintain an inventory buildup state, with next week's aluminum billet inventory expected to operate between 150,000-180,000 mt.

Regarding processing fees, this week SHFE aluminum first fell then rose, with the spot price center still fluctuating at highs above 20,500. The slight pullback in the price center in the first half of the week stimulated some just-in-time procurement, but the subsequent rise in the price center again suppressed consumption, with some markets once again entering a "negative processing fee" state. However, as the reduction in aluminum billet production continues to expand, suppliers are intentionally refusing to budge on prices, and the processing fee center is gradually rising. As of July 10, 2025, the aluminum billet market in the Foshan area was quoted at 30/80, up 60 from last Thursday; the processing fee in the Wuxi area was quoted at 110/160, up 40/20 from last Thursday; the processing fee in the Nanchang area was quoted at -30/20, up 60 from last Thursday. In summary, the current aluminum billet market is in a state of oversupply, with persistently low processing fees also indicating weak consumption. In the short term, it is difficult to see an increase in consumption, while the available supply of aluminum billets continues to grow. It is expected that in the short term, aluminum billet processing fees will mainly remain in a weak consolidation.

》Order to view historical spot prices of SMM metals

》Click to view SMM aluminum industry chain database